Following May’s local election results, political uncertainty has unsettled the UK bond market. Speculation about the future of Prime Minister Sir Keir Starmer and Chancellor Rachel Reeves has contributed to rising government borrowing costs, pushing gilt yields to some of their highest levels in decades.

With the Prime Minister’s long-term future now in doubt, investors are growing increasingly nervous about the direction of the government’s fiscal policies.

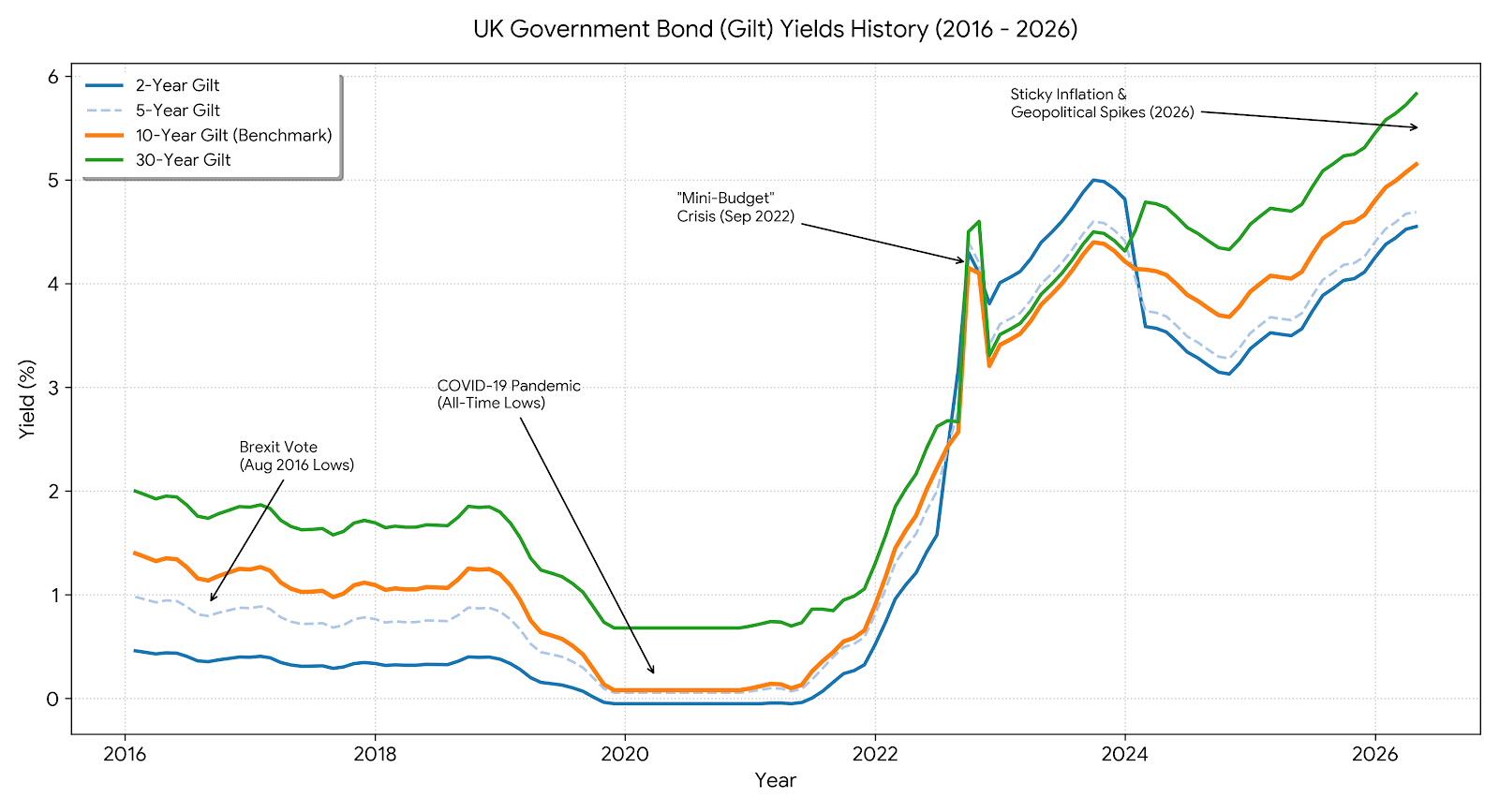

Concerns that a shift in political leadership could result in higher borrowing to fund public spending have sparked a bond sell-off. Compounded by worries over inflation and geopolitical tensions from the Iran War, the yield on 30-year debt—which moves inversely to price—has reached its highest level since 1998.

Gilts are British government bonds. When investors buy a gilt, they are effectively lending money to the state in exchange for regular interest payments (known as coupons) and the return of their original principal when the bond matures.

While UK gilts were once deemed one of the safest havens for capital, they have recently become unnervingly volatile. The UK’s growing reputation for political unpredictability has driven up borrowing costs, pushing them to the highest levels in the G7.

Yet, as with any period of market volatility, this environment creates both risks and unique opportunities for investors.

Why investors are concerned

If the government increases borrowing it must issue more gilts to raise money. This greater supply can push down the price of existing bonds, particularly older ones paying lower coupons.

Investors are demanding higher yields to compensate for concerns over the UK’s economic policies and growing national debt burden which has climbed significantly since the 2008 financial crisis.

Inflation remains another key risk. Prior to the outbreak of the Iran War, UK inflation was already proving persistent at 3%, compared to just 1.9% in the euro area.

As the conflict sent oil prices climbing, inflation expectations naturally rose with them. This spike forced gilt yields even higher as traders abandoned bets on imminent interest rate cuts, pricing in the possibility of further rate increases instead.

The Bank of England may keep interest rates higher for longer or even raise them further. Higher interest rates typically reduce the value of existing bonds because newly issued gilts offer much more attractive returns.

Long-dated gilts are particularly vulnerable to this effect. A small change in interest-rate expectations can cause significant swings in their value, a risk known as duration risk.

Why gilts may look attractive

Rising yields mean new investors can lock in higher levels of income than were available a few years ago. Many older gilts issued when interest rates were close to zero have fallen sharply in value, allowing investors to buy them at significant discounts to their £100 face value.

For investors who hold these bonds until maturity, there is potential to receive both the regular coupon payments and a capital gain as the bond is repaid at its full face value.

Importantly, gains made on directly held gilts are exempt from Capital Gains Tax (CGT), making them particularly attractive for investors who have already used their ISA allowance.

Short and medium-dated gilts are currently favoured by many wealth managers because they offer relatively attractive yields while being less sensitive to future interest-rate movements than longer-dated bonds.

The bottom line

Gilts continue to offer a relatively secure source of income backed by the UK government, which has never defaulted on its debt. Higher yields and tax advantages mean there are opportunities for investors willing to hold bonds to maturity.

However, political uncertainty, rising government borrowing and the possibility of higher inflation or interest rates could lead to further volatility.

Investors considering gilts should understand that while they are generally less risky than shares, they are not risk-free and their value can fall significantly before maturity.